I Just Found Coverage For Half Price: Here's why...

Half price. Same coverage. That’s the pitch.

Here’s the truth: it’s a lie.

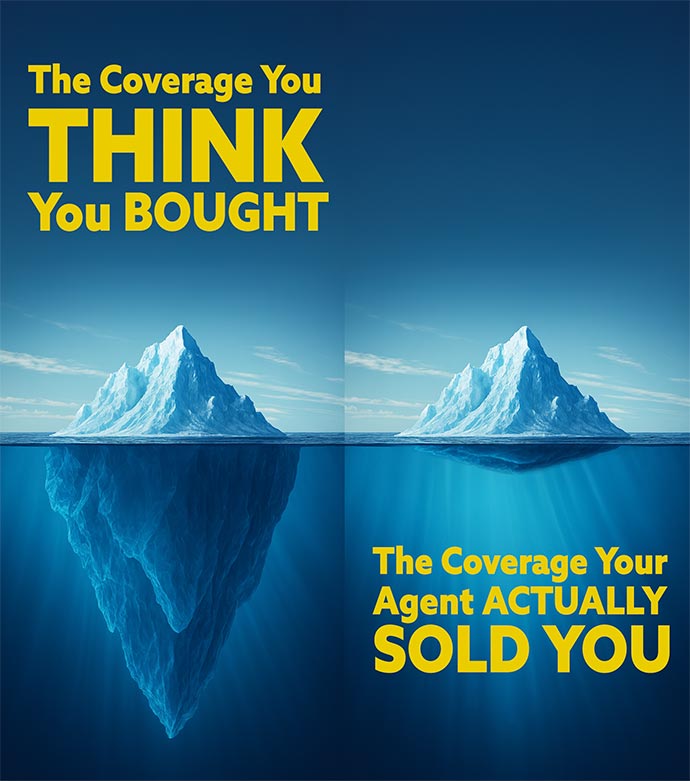

When an agent hands you a “too good to be true” quote, they didn’t magically outsmart the system. They gutted your coverage, misrepresented your business, or both. That’s not savings. That’s sabotage—of your protection, your reputation, and your bottom line.

1. Limits gutted to look “competitive”

A million-dollar claim doesn’t stop at $300,000. But that’s what the half-price policy buys you: a ceiling so low the first lawsuit punches through it. The other side collects. The carrier walks away. You’re left holding the bill. That “cheap” premium? It just turned into a six-figure loss.

2. Endorsements cut without warning

The protections that matter most to your business—tools, subcontractors, completed operations, hired/non-owned autos—vanish in the fine print. The policy “covers” you in theory, but not in the scenarios that ruin companies in reality. By the time you find out, the adjuster is already shaking their head.

Get A Quote

3. Risk misrepresented to the carrier

This is where agents cross the line from sloppy to reckless. They fudge your payroll. They downplay your operations. They make your business look safer than it is. Why? To shave dollars and steal your account.

But when the carrier audits—or a claim exposes the lie—coverage collapses. You’re left naked, the carrier is furious, and the agent is staring down lawsuits and license loss. Everyone loses.

4. Exclusions slipped in where you’ll never look

The half-price trick is simple: bury exclusions for water damage, subcontractor work, equipment breakdown, or professional liability. They’ll tell you “it’s standard.” It isn’t. They know most clients never read page 47 of the policy jacket. You’ll discover the truth the day a denied claim costs more than a decade of “savings.”

5. The fallout hits harder than the discount

Cheap insurance doesn’t just fail you—it poisons the industry. Carriers are left holding risks they never agreed to. Honest agents look overpriced for telling the truth. And business owners lose faith in all of us. Every dishonest quote doesn’t just wreck one client. It wrecks trust across the board.

Call Us Now

The bottom line

A policy isn’t a coupon. It’s a contract. When it’s cut in half, it’s not a bargain—it’s bait.

If your agent hands you a half-price quote, ask yourself: What did they cut out? What did they hide? What lie did they tell to make this look cheap?

Because here’s the rule:

If you don’t pay for coverage now, you’ll pay for losses later. With interest.

FAQ: The Hard Truth About Half-Price Policies

Because something is missing. Lower limits, stripped endorsements, buried exclusions—or an outright lie told to the carrier about your risk.

Yes. If your application doesn’t match reality, the carrier has every right to deny coverage. One denied claim can end your business.

Not when the “savings” is a few thousand and the risk is millions. That’s not savings—that’s gambling your company’s future for lunch money.

Everyone. You face denied claims. The carrier faces unplanned losses. The agent risks lawsuits and license loss. No one wins.

Don’t ask, “Is it cheaper?” Ask, “What’s missing? What’s excluded? What’s misrepresented?” If the other agent can’t answer directly, you already know.